How much are you really paying for Financial Advice?

Using a financial advisor is a surefire way to increase your return on investments and subsequently, your savings and pension funds etc.

But, how much are your really paying? Is it worth it? And, how much do you understand about what’s going on with your finances?

This is where a portfolio analysis is your most useful tool. If you hold an offshore investment bond or expat investment vehicle, the chances are that you are not having the performance regularly reviewed or that the financial adviser that sold you the investment bond or platform is no longer interested in helping you out.

What is a Portfolio Analysis?

Simply put, a portfolio analysis looks at a person’s portfolio of savings, investments, pensions and everything in between. It’ll help to identify hidden costs and how they impact your overall returns. Appropriateness of each element of your portfolio will also be examined – keeping you, the client, in control.

Why a Portfolio Analysis is so important.

Portfolio Analysis puts you in control of your finances. By identifying hidden costs you can look to change your advisor or policy in order to reap the benefits that your money is producing. As well as this, the liquidity of your portfolio will be assessed i.e. how quickly you can access your money if you needed to and further ways to increase your returns will be discussed.

Costs.

Of course, there are costs to using a financial advisor. You have to spend money to make money right? Well, whilst this is true it doesn’t necessarily mean you must give away half your fortune. Nor does it mean that the most expensive advice is the best. This is when a few question must be asked: Is my financial advisor fee-based or commission-based and is my money being used for active or passive investments?

Equally, you must question what the fees are actually funding. Many financial advisors will advertise astonishingly low fees. However, this proclamation of low costs does not necessarily mean more money for you. Keep reading to find out why…

Commission v Fee.

A Commission-Based service means an advisor will essentially be paid for the amount of transactions and services he executes. This means they are directly incentivised to make as many trades as possible – whether good or bad for the client.

A Fee-Based advisor on the other hand will benefit more from their clients wealth growing. Meaning they are directly incentivised to increase the client’s wealth.

Exchange-Traded Funds

Exchange-Traded Funds (ETF) are the prime reason why advisors can advertise an extremely low fee. ETFs are an investment tool which, essentially, follow the market. Meaning your returns will follow the market. This sounds great, right? Your money is pretty secure and you’re making more than you would in the bank. Sure. But, consider this: the advisor you’re paying is not doing anything with your money; whilst the market is increasing by 3 or 4% some stocks (e.g. Fever Tree) are increasing by 25%; and, these low-fee funds often come with a huge ‘get out’ fee.

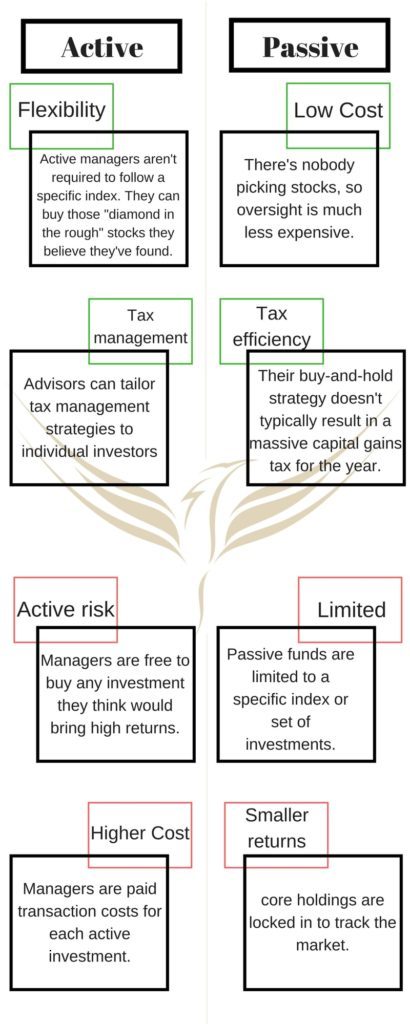

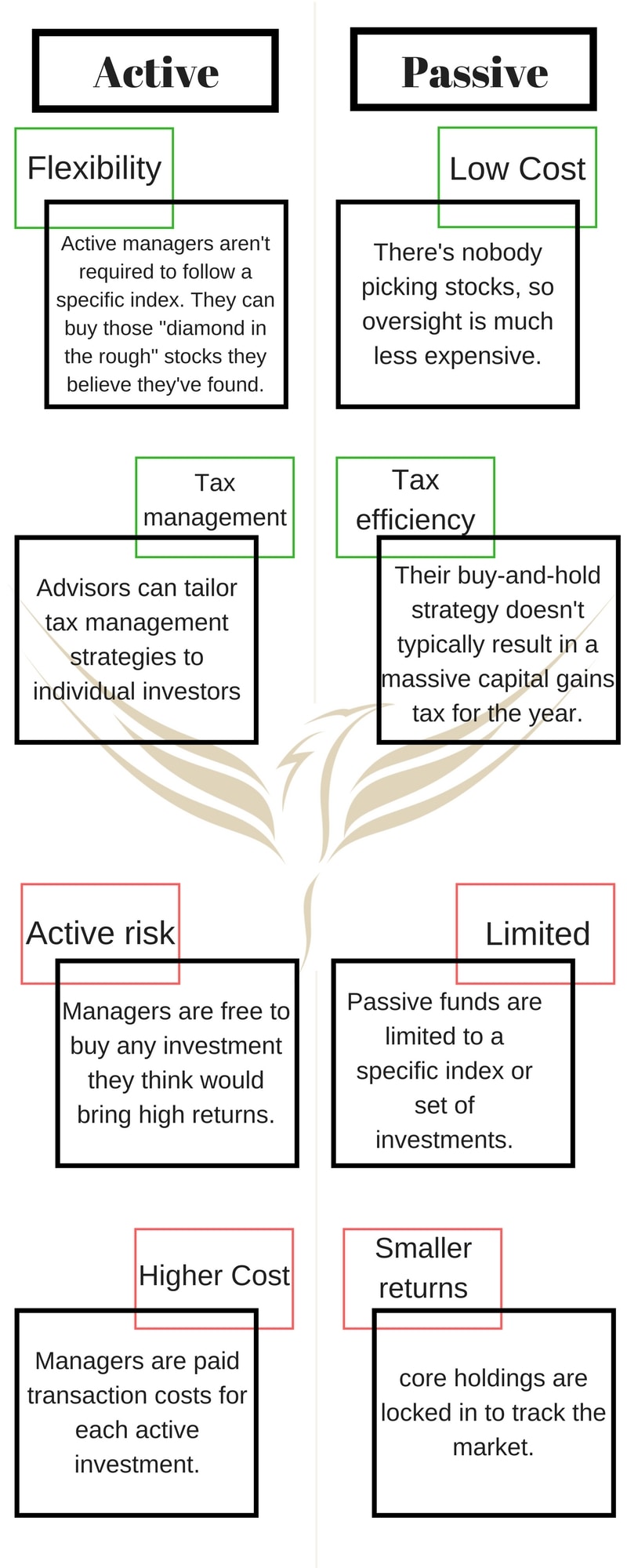

Active or Passive Investing

This brings us on to methods of investment. A portfolio analysis will tell you how your money is being invested, and whether this is inline with your tolerance toward risk.

Active Investing simply means that your financial manager is committed to seeking out funds which are believed the create the greatest returns.

Passive Investing aims to keep buying and selling to a minimum. ETFs are an example of a passive investment.

So here are some of the key features, strengths and weaknesses of Active and Passive Investing:

For a full Portfolio Analysis and advice on what is best for you and your money, contact us today.

neetandjames@hotmail.com Anita Green International SIPP GBP